School is starting, the weather is changing – it’s almost time for Football. So let’s take advantage of a nice weekend and think about finances.

Geraci Law has the tools to help! It does not matter if you are trying to figure out a savings plan or if it’s time to take a good hard look at what your expenses are. If you are seeing on the monthly budget that you are operating in the negative – it might be time to realign.

So pick out your favorite cold one, grab a calculator (there’s one on your iPhone) and let’s figure out your budget!

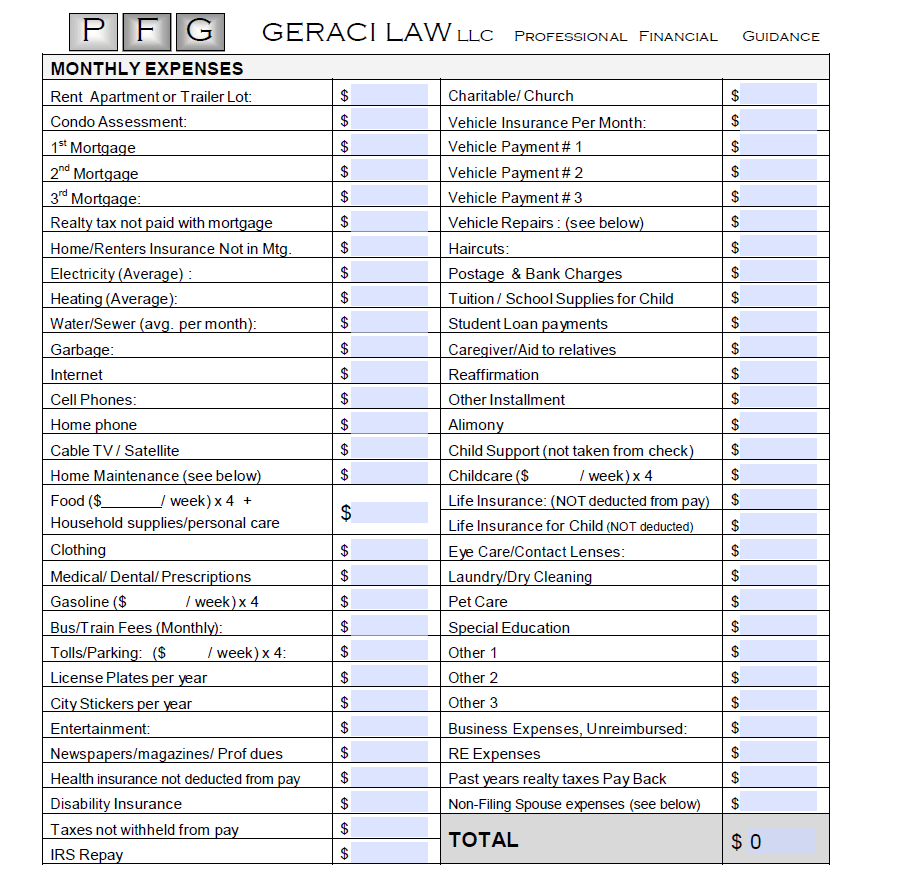

Check out below. You can fill in your monthly expenses. Take note – your Starbucks coffee (a beverage part of budgeting) should list under Entertainment. Tip: go to your bank account and look how much you are spending each month.

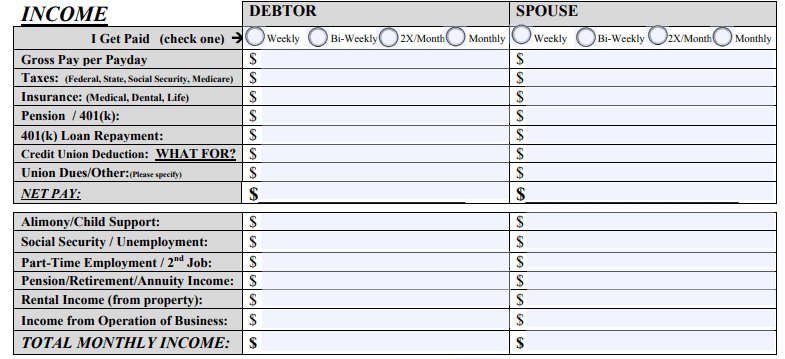

Next – let’s take a look at your income. You can use this as a guide! Tip: if you are paid salary, use one paycheck since your income does not change. If you are paid hourly, take the average of the last 3 months.

After that, take the amount in TOTAL MONTHLY INCOME and subtract from your Total from the monthly expense worksheet….

THIS is your disposable income – it’s the amount you have left at the end of the month to either save or spend.

When you have debt including credit cards, Pay Day loans, medical bills (note bill NOT expense) the minimum payment is substracted from your disposable income NOT from your expenses.

If the amount is high and you are not paying DOWN the balance on the debt, reexamine the budget. Go back to the disposable income amount – if you eliminate the debt payment, this is the money that goes back to YOU.

If you have $1,000 in disposable income every month and are paying $1,000 in minimum payments – if you are then using your credit card to pay the monthly expenses (from the first worksheet) your plan is NOT working.

Instead if you account for the monthly expenses where you can pay for the bill without relying on credit, you have disposable income to put into a savings account. $1,000 per month for 12 months is $12,000 an amazing start to retirement, paying for college, down payment on a home, etc.

Dial 1-800-CALL-PFG for a free phone mini-consultation, or make an appointment online 24/7 at www.infotapes.com. Bankruptcy laws are in place to help you. Who knows bankruptcy like Geraci Law? Geraci Law has 30,000 5-star reviews ![]() since November 2016!

since November 2016!

Read ALL ABOUT DEBT RELIEF at www.bankruptcybookbypeterfrancisgeraci.com.